The Best Way to Implement New Technology into Your Mortgage Process

Technology is reshaping the mortgage industry from the ground up. No longer is digital transformation a luxury—it’s a competitive necessity. Borrowers expect a seamless, fast, and transparent process. Lenders expect cost savings, improved compliance, and scalability. Yet many organizations struggle with how to integrate new tools into their mortgage workflow without disrupting operations or losing the human element that drives trust and retention.

Whether you’re a regional lender or a national operation, the best way to implement new technology is not to chase trends—but to build a thoughtful, phased strategy that enhances every stage of the loan lifecycle.

Let’s break down how mortgage professionals can implement digital tools that streamline everything from borrower intake to underwriting, income verification, closing, and post-close servicing—without compromising compliance or borrower satisfaction.

For lenders of any size, the right technology strategy should work with existing systems, automate where it counts, and help teams do more with less—while keeping the borrower experience front and center.

Why Mortgage Tech Matters More Than Ever

The average time to close a mortgage is still around 40 to 45 days—an eternity in the age of instant everything. But the problem isn’t just consumer frustration. Slow turnarounds, redundant manual work, and outdated verification processes contribute to higher origination costs, loan fallout, and compliance risks.

On the flip side, lenders who adopt integrated digital systems report measurable gains:

- Up to 30% cost reduction in loan processing

- 20–25 days shaved off the closing timeline

- Improved borrower retention and net promoter scores (NPS)

- Fewer compliance violations thanks to automated data checks

As regulatory scrutiny grows and fraud risks evolve, digital transformation is no longer just about keeping up—it’s about protecting the business and positioning it for long-term success.

Step 1: Start with the Borrower Experience

The mortgage process begins at the point of sale—and so should your digital transformation. A modern point-of-sale (POS) system enables borrowers to:

- Complete digital applications on any device

- Securely upload documents

- Link their bank, payroll, and tax information

- Communicate with loan officers in real time

When tightly integrated with the loan origination system (LOS), a modern point-of-sale (POS) system does more than streamline data entry—it becomes a launchpad for intelligent automation and risk mitigation. By embedding credit pulls, income and asset verifications, and data quality checks directly into the initial application flow, lenders can validate critical borrower information in real time. This early insight allows for faster identification of documentation gaps, eligibility concerns, or red flags, long before a file reaches underwriting.

The result: underwriters receive more complete, accurate files from the start—reducing time spent on rework, resubmissions, and manual data validation. This early-stage precision not only accelerates the underwriting process but also reduces fallout risk, improves cycle times, and strengthens overall loan quality.

New technologies now enable these early checks to run automatically in the background, using configurable rules engines and API-driven integrations to ensure consistency and compliance without slowing the borrower’s experience. As regulatory requirements grow more complex, and as borrowers expect faster decisions, this kind of early automation is becoming a critical advantage—not just operationally, but strategically.

The operational impact is significant. Loan officers, processors, and underwriters spend less time chasing documents, correcting errors, or manually re-verifying information—freeing them to focus on high-value tasks like exception handling and borrower guidance. Automation reduces bottlenecks across departments, while consistent data flows minimize back-and-forth between systems. This not only boosts productivity and throughput but also lowers per-loan costs in a margin-sensitive environment.

At the same time, borrowers benefit from a faster, more transparent experience. Applications move forward with fewer delays. Communications are more streamlined. And because verifications happen in real time, borrowers receive earlier clarity on their loan status—building confidence and reducing the frustration often associated with long wait times and unexpected documentation requests. In a market where customer expectations are higher than ever, this kind of experience can be a key driver of loyalty and retention.

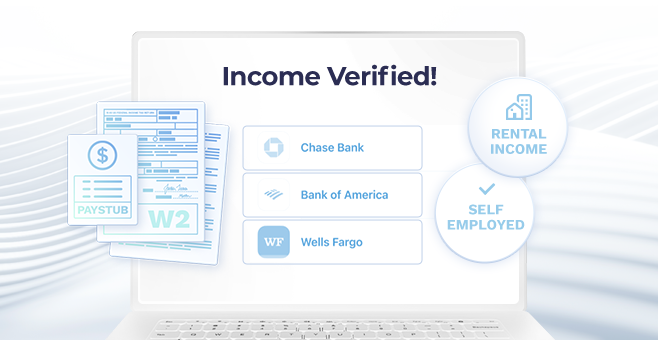

Step 2: Automate Income and Employment Verification

Automated Income and Employment Verification: From Risk to Opportunity

Manual income and employment verification remains one of the most outdated—and highest-risk—steps in mortgage origination. Relying on uploaded pay stubs, employer letters, or tax returns introduces delays, errors, and potential document fraud, slowing the process and increasing risk.

Today’s digital verification solutions allow borrowers to securely connect payroll systems or financial accounts directly, enabling near-instant, automated confirmation of:

- Employment status and history

- Base salary, bonuses, and commission structures

- Tax filings and historical earnings

By eliminating manual document collection and labor-intensive reviews, lenders accelerate pre-approval and reduce underwriting conditions. These technologies also accommodate self-employed and gig economy borrowers through advanced income modeling and alternative data sources.

Lenders adopting automated income and employment verification often see timelines shrink from several days to under an hour—dramatically improving the borrower experience. Beyond speed, these solutions improve data accuracy and reduce repurchase risk by providing lenders with verified, auditable income evidence early in the loan lifecycle.

When verification is integrated from the point of sale through underwriting, lenders build stronger, more efficient workflows that enhance compliance and borrower trust throughout the entire mortgage process.

Step 3: Embrace AI-Driven Underwriting

Modern Underwriting Starts at the Point of Application—Powered by Intelligent Automation

Underwriting remains one of the most labor-intensive and time-consuming steps in the mortgage process. Traditionally, underwriters manually sift through credit reports, income documents, assets, and collateral—often juggling multiple systems and dealing with inconsistent file quality.

Today’s technology changes the game by embedding AI and rule-based automation early in the workflow, starting at the point of sale and application. This approach ensures that the data entering underwriting is already verified and standardized, enabling underwriters to focus on what matters most.

Here’s how AI-enhanced underwriting works:

- Automatically scans and verifies documents for accuracy, completeness, and fraud indicators

- Assesses borrower eligibility based on up-to-date program guidelines and credit overlays

- Flags anomalies or edge cases for expert human review

- Recommends approval, counter-offer, or decline decisions based on configurable rules

The benefits are clear. Underwriters handle cleaner, more consistent files and spend less time on routine tasks—allowing them to resolve complex exceptions faster. Lenders leveraging these AI-driven systems report up to a 70% reduction in underwriting turnaround times, fewer touches per file, and greater decision consistency.

Importantly, these underwriting engines can be configured to comply with Fair Lending requirements and other regulations by documenting decision logic and providing complete audit trails—ensuring that speed doesn’t come at the expense of compliance.

By integrating these technologies from the earliest borrower interaction through to final underwriting decisions, lenders build a more efficient, accurate, and risk-aware mortgage process that benefits both teams and borrowers alike.

Step 4: Digitize Appraisal, Title, and Closing Workflows

Even when underwriting is efficient, delays often occur during the back half of the loan process. Appraisals, title work, and closings are frequent chokepoints. Here’s how emerging tech can help:

- Property Valuation: Desktop appraisals and hybrid models use public data, listing platforms, and limited inspections to deliver accurate valuations faster. Automated valuation models (AVMs) are increasingly accepted for certain loan types.

- Title & Settlement: Digital title workflows streamline searches, clear liens faster, and provide real-time updates. Lenders can track title progress without constant emails and phone calls.

- eClosing & RON: Remote online notarization (RON) and full eClosings allow borrowers to review and sign documents virtually, reducing closing timelines from days to hours. These tools also simplify the funding and post-closing processes with instant document delivery and tamper-proof audit trails.

The Mortgage Bankers Association (MBA) predicts that by 2026, over 60% of closings will involve digital components. Many lenders have already shortened closing time frames by 3–5 days with even partial digital adoption.

Step 5: Use Automation in Post-Close and Servicing

Loan Quality Doesn’t Start at Post-Close—And It Shouldn’t End There Either

Modern lending technology enables quality control to begin at the point of sale—long before the loan reaches post-close. With real-time data validation, automated verifications, and integrated underwriting logic embedded at the application stage, lenders can reduce defects early, improving loan quality and minimizing costly downstream rework.

But the opportunity doesn’t stop at closing.

Post-close automation ensures that quality, compliance, and borrower experience continue long after the ink is dry. AI-powered tools now support a smarter, more proactive approach to loan management and servicing:

- Automated post-close QC that flags document discrepancies, missing signatures, or funding issues before loans hit investor review

- AI-driven chatbots that handle borrower inquiries around payments, forbearance, or escrow—reducing call center volume and improving satisfaction

- Predictive servicing models that identify risk signals early and help servicers proactively engage borrowers before delinquency occurs

These tools do more than reduce operational cost. They help lenders protect loan salability, reduce repurchase risk, and maintain strong borrower relationships throughout the life of the loan. In an environment where margin, compliance, and customer experience all matter, quality can’t be a back-end task—it must be embedded from the first borrower click to the final payment.

Keys to a Successful Implementation Strategy

A Phased Approach: Implementing Technology Without Disrupting Operations

For many lenders, the biggest barrier to modernization isn’t the technology—it’s the fear of operational disruption. Legacy systems, compliance requirements, and entrenched workflows can make the idea of sweeping change feel risky. But the most successful digital transformations aren’t all-at-once overhauls—they’re phased, intentional, and aligned with real business needs.

The first step is identifying high-friction areas in the loan lifecycle—such as borrower intake, income verification, or document management—and targeting those with focused technology investments. These early wins create immediate impact while minimizing risk. Modern platforms are increasingly modular and API-driven, meaning lenders can layer new capabilities on top of existing infrastructure rather than ripping and replacing core systems.

Change management also plays a key role. Training, communication, and clear performance metrics ensure that staff not only adopt new tools, but use them effectively. Lenders that treat transformation as a collaborative process—between operations, compliance, IT, and the front line—are better positioned to sustain momentum and scale innovation over time.

Ultimately, the goal isn’t just to digitize the mortgage process—it’s to make it smarter, faster, and more resilient without compromising control, compliance, or the borrower experience.

Even the best technology fails without a clear roadmap. Here’s how mortgage professionals can successfully implement digital tools.

Build for ROI, Not Just Relief

Start Where ROI Is Highest

Digital transformation doesn’t require a full-system overhaul on day one. Focus first on the areas where technology can deliver measurable return—like reducing time to close, cutting touches per file, or increasing pull-through rates. Early wins build momentum and justify continued investment.

Ensure Seamless Integration

Select solutions that are built to integrate—with your LOS, document systems, and third-party services. Look for platforms that use open APIs, standardized data formats, and native integrations. Your LOS should act as the central hub of a connected, efficient ecosystem—not a bottleneck.

Empower Teams Through Training

Even the best technology underperforms without user buy-in. Invest in onboarding, provide practical training tailored to each role, and highlight real-world wins to reinforce value. Underwriters, processors, and loan officers should feel supported, not sidelined.

Track What Matters

Establish clear performance benchmarks—such as reduced cycle times, higher NPS, or fewer manual touches—and measure results over time. Use data to refine implementation, expand intelligently, and continue improving ROI with each phase.

Keep Compliance Aligned

Bring compliance into the conversation from the beginning. Modern tools should improve regulatory adherence through audit-ready data capture, real-time checks, and system-enforced consistency. Choose technology partners who treat compliance as a built-in feature, not an afterthought.

Final Thoughts: It’s Time to Think Holistically

Technology That Works With Your Team—Not Around It

Implementing new technology isn’t just about adopting the latest tools—it’s about building a connected, intelligent ecosystem that accelerates workflows, improves decision accuracy, and reduces risk at every stage of the mortgage process.

From automated income and asset verifications to AI-supported underwriting, eClosings, and predictive servicing, the components of a future-ready mortgage operation already exist. The real advantage lies in how they’re implemented—strategically, and in ways that empower teams like underwriting and processing to work more efficiently, not harder.

Success starts with a clear roadmap: choose technologies that integrate seamlessly with your existing systems, support compliance, and reduce manual touchpoints without sacrificing control or judgment. The goal isn’t to replace people—it’s to equip them with tools that drive better outcomes, faster.

Lenders who invest in this kind of transformation aren’t just reducing costs—they’re improving file quality, cycle times, and borrower satisfaction. And that translates into something every lender and underwriter can appreciate: stronger performance, less rework, and a competitive edge that compounds over time.